English

English 日本語

日本語 繁體中文

繁體中文 簡體中文

簡體中文 Русский

Русский 韓文

韓文Corporate Governance

Internal Audit Organization and Operations

Internal Audit Organization

1. The Audit Office of the Company is an independent unit under the Board of Directors. Any appointment or dismissal of a chief internal auditor is subject to approval by the Board of Directors. The chief internal auditor is responsible for submitting the appointment or dismissal, evaluation and remuneration of internal auditors to the Chairman of the Board for approval

2. The Company has qualified and full-time internal auditors and deputies in place. The Company reports in a prescribed format to the authority in charge for recordation on a regular basis.

3. The Company's internal auditors meet the statutory qualifications and pursue continuing education to improve their knowledge and skills.

Internal Audit Operations

1. The Audit Office carries out internal audits to assist the Board of Directors and executives in inspecting and reviewing defects in the internal control system as well as measuring operational effectiveness and efficiency, and makes timely recommendations for improvements to ensure the sustained operational effectiveness of the internal control system.

2. The internal auditors are detached, independent, objective, and impartial, in faithfully performing their duties, and exercise due professional care. The chief internal auditor reports the audit operations to the Audit Committee on a regular basis and also attends and delivers a report to a Board of Directors meeting.

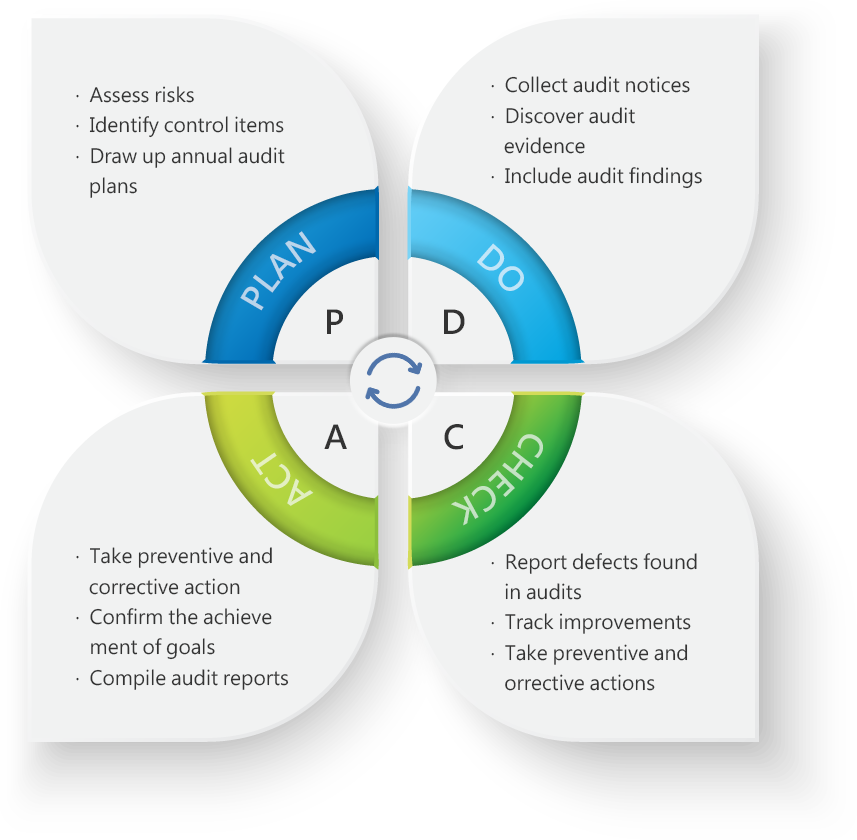

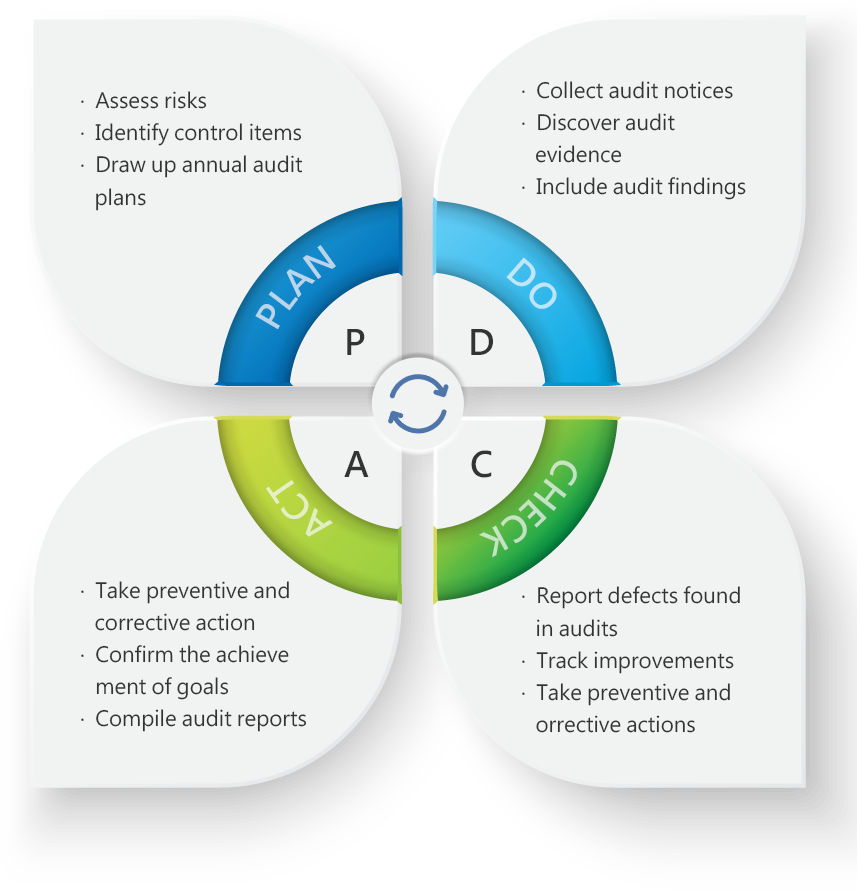

3. Scope of internal audits: (1) The Rules for the Implementation of Internal Audits stipulate that internal auditors review the internal controls of the Company’s operating procedures, and report whether the design and daily operations of such controls are appropriate, effective, and efficient; the scope of internal audits covers all units, operations and subsidiaries of the Company. (2) Internal audits are implemented according to the audit plan approved by the Board of Directors, which is based on the identified risks. Special audits are implemented as needed to check whether the Company's internal control system is appropriate, effective and efficient. A special audit report is prepared and submitted to each independent director for review. (3) Internal auditors review the self-assessments implemented by the Company's units and subsidiaries, including checking whether the self-assessments are implemented and reviewing documents, to ensure the quality of the implementation. The results of the self-assessments are synthesized and reported to the Audit Committee and the Board of Directors.

4. Internal auditors report the audit operations to the authority in charge before the statutory time limit.

Internal Audit Process – PDCA Cycle