公司治理

內部稽核組織及運作情形

一.內部稽核組織

1. 本公司稽核室為一獨立單位,隸屬於董事會,內部稽核主管之任免必須經董事會同意。內部稽核人員之任免、考評、薪資報酬由稽核主管簽報董事長核定。

2. 目前配置符合適任條件及專職之內部稽核人員,並設置職務代理人,定期依主管機關規定格式,申報備查。

3. 本公司內部稽核人員之資格符合法定之適任條件,並持續進修專業知識及技能。

二.內部稽核運作

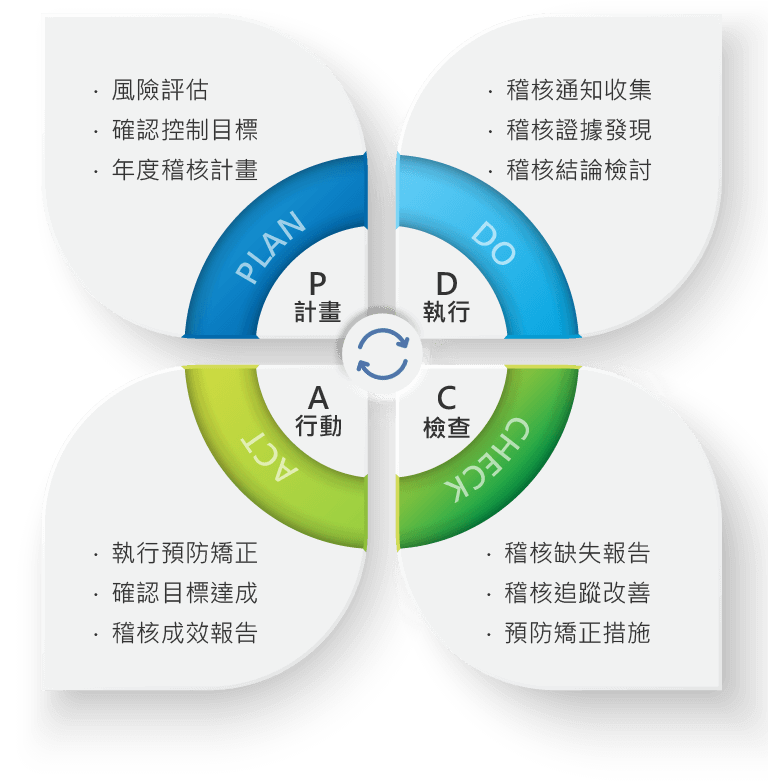

1. 稽核目的在於協助董事會及經理人檢查及覆核內部控制制度之缺失及衡量營運之效果及效率,並適時提供改進建議,以確保內部控制制度得以持續有效實施。

2. 內部稽核人員秉持著超然獨立之精神,以客觀公正之立場,確實執行職務,並盡專業上應有之注意,稽核主管定期於審計委員會報告稽核業務,並列席董事會報告。

3. 內部稽核及服務範圍: (1) 內部稽核實施總則明訂內部稽核覆核公司作業程序的內部控制,並報告該等控制之設計及實際日常運作是否適當及兼顧效果與效率;其覆核範圍涵蓋公司所有單位、作業及子公司。(2) 依據董事會通過的稽核計畫執行,該稽核計畫乃依據已辨識之風險擬訂,另視需要執行專案稽核,據以檢查公司之內部控制制度是否適當及其效果和效率,並作成稽核報告呈核,交付各獨立董事查閱。(3) 內部稽核覆核公司各單位及所有子公司所執行的自行評估作業,包括檢查該作業是否執行並覆核文件以確保執行的品質,並綜合自行評估結果,報告審計委員會及董事會。

4. 內部稽核人員於法定時限前,向主管機關辦理申報各項稽核業務。

稽核運作流程 - PDCA 循環